Delivering a password

Posted On Feb 19, 2008 at by Prakash G.R.2 months back, after the normal password change stuff, I forgot the new password of my ICICI Demat account. I applied for a new password thru the portal, but it was returned back saying invalid address. After 5 mins of waiting and a long call with the customer care "executive", I got them resend the password. It was sent back again for the same reason. It happened twice again. The last time, I was not ready to take chance. I followed up with the First Flight couriers and I was going there to the Peelamedu office every day and finally got my password - nearly after 2 months!(for a change, this time the mistake was not by ICICI)

When I asked them what was wrong with the address, I got this stupid answer: One of the delivery guys went for a long leave and they didn't have enough resources. And more over the password was sent in a ZB category, which means they should not hold it for more than a day or two. So they sent it back. The best reason to return it was to say that the address is invalid. WTF? When I asked whether they know how important the timely delivery of a demat account password, I got a sarcastic answer. I really got pissed off, but shouting there is of no use. I decided to hit them where it hurts.

Back to home and the first thing I did was to write a detailed mail to ICICI's helpdesk about what happened, and put the First Flight's Mumbai head office & regional head office in the CC. I said not to deliver any of the communication to me thru this courier and suggested them not to use this for anyone else also. The response was good. The FF Courier's head office guys contacted me for more info of what happened. After 2 days (probably probing into what exactly happened) they apologized and said it will not happen. I hope the Peelamedu guys would have got whatever they deserved or even more.

PS: In case you were wondering, the help desk guy @ ICICI direct did what he was trained to. He replied (luckily not Reply All) promptly with the step-by-step directions of how to apply the new password. I replied asking him to forward the issue to their superiors and take appropriate action. That worked. At least their supervisor could understand and promised me that they will take up the issue to concerned authorities in ICICI and thanked for the feed back.

How to choose a housing loan?

Posted On Jan 4, 2008 at by Prakash G.R.A lot many of us know this one, mostly after a painful experience in some way or other. This are few tidbits that I've learnt thru my own experience and thru my friends' experience.

- After you have decided on the house/apartment, check whether any banks have approved the project. If a bank has it approved then your paper work becomes much easier with that bank.

- Period of loan plays a very important role. There is no very big difference in EMI for a 20 year loan and 10 year loan. It would be ~ Rs 100 per 1L. So if you are taking a loan for 10L, a 10 year loan will result in Rs 9000 EMI and 20 year loan will result in Rs 10000 EMI. The trade-off is between paying a little high every month for 10 years or paying less for 20 years. In any case, as a rule of thumb, make sure your EMI doesn't cross 40% of your take-home pay.

- The choice between interest types - floating/fixed is always confusing for many. The floating interest rate went all the way to 7% few years back and now its back to 11%. Whether it will decrease/increase in the next 20 years is hard to predict. Also the fixed is not really fixed. The banks can change that rate also. Some banks allow switching between these two. Many banks offer a combination of two - fixed for first 5 years and floating for the rest of the period. Look for these options

- Not all of the banks will give you the whole amount. You have to bring in around 10-20% and the bank will lend the rest. However, you can find some deals with the banks for lending the whole amount. If you don't have cash for the down payment and not very keen in opting for a personal loan, this might be a good deal. The penalty of taking 100% loan is the interest rate will be a little higher (but will be definitely less than the personal loan's interest rate)

- Processing fee is another charge that you have to pay. It ranges from a fixed amount of Rs 5,000 to 2% of the property value. In some loan mela or exhibitions or some festive offers, banks usually levy off this fee. That means you can negotiate for the same during other time as well. Talk :-)

- Till the construction is over, you need to pay a Pre-EMI. Remember this Pre-EMI doesn't include any principal amount. So if your construction takes 2 years, all two years, you will be paying only interest and not a single Re for your principal. There are two alternatives for this. One is that you can pay as Tranche EMI, which includes the principal amount also. This is applicable for only the amount that has been disbursed to the builder. The second option is to start the EMI right from the first month. In both cases, the principal amount repaid cannot be used to reduce your tax. Many banks allow you to change the scheme for a nominal charge/free of cost.

- Be cautious about part-prepayment. Say you get a bonus of 2L and you wish to pay it towards your home loan so your monthly EMI burden comes down. After you have paid the amount you may not see any change in the EMI. This might be because many banks take the part-prepayment into account only in the end of the quarter. If you think that is bad, some schemes in ICICI bank do at the end of the financial year! That means if you pay 2L on Jun 07, that is no use of you till Apr 08. On the nice side, most of the schemes in SBI does it on the very same day you paid the amount. You will have restrictions like you can't pay more than half of your principal left, the minimum amount should be more than 3 EMI, you can pay only once in an year and so on. On top of it all, they might also charge you a part-prepayment penalty. Its usually less than 5%, but on which the % is calculated sometimes differs. Few banks will charge that percentage on the amount you pay and few on the whole amount. Double check that before opting for a loan. For all schemes in HDFC (not HDFC Bank, its HDFC) its 0%!

Know any more suggestions? Leave a comment.

A credit card story

Posted On Dec 31, 2007 at by Prakash G.R.You would have heard of several horror stories about Credit Cards. How the banks cheat you, over charge you, abuse you etc. Here is a nice story of a Credit Card.![]() I got a HFDC Card 3 years back. I used it to pay monthly utilities like phone & internet and used it for other purchases as well. Once I started using it, the advantage of Credit Card is apparent. My billing cycle of mobile is 26-25. So I get a bill sometime around 30th of every month and the last date is somewhere around 15th. I pay it by 10th with my Credit Card. My credit card's billing cycle is 10-9. So the transaction will come only in the next month's Credit Card bill. I've to pay that only 20th of next month. So I talk in August and actually spend for that only in October!

I got a HFDC Card 3 years back. I used it to pay monthly utilities like phone & internet and used it for other purchases as well. Once I started using it, the advantage of Credit Card is apparent. My billing cycle of mobile is 26-25. So I get a bill sometime around 30th of every month and the last date is somewhere around 15th. I pay it by 10th with my Credit Card. My credit card's billing cycle is 10-9. So the transaction will come only in the next month's Credit Card bill. I've to pay that only 20th of next month. So I talk in August and actually spend for that only in October!

Big purchases are another good thing. I usually convert them into EMIs. I get them after 10th and convert them into EMIs. When you convert into EMI, the transaction will appear in the current month's statement but the EMI will start in the next month's statement. I don't know whether its a feature or a quirk in their system, I don't want to complain anyway. So I don't get to pay a single paise out of pocket for two months, yet enjoy watching my TV.

I always pay before the due date, so I never went into any sorts of troubles. The good part is I get reward points for all my expenditures. HDFC Bank has a huge list of items to redeem your points for. Last month I opted for Tata Sky. I've to pay a Rs 1,700 extra, but I'll get gift coupons worth of Rs 1,500. That effectively means, I pay Rs 275 (adding the shipping charges) for the Tata Sky. Thats a good deal. Tata Sky guys came in, installed and said that I got 6 months subscription free (its a new deal from Tata Sky for every purchase of Tata Sky), so I have to pay only the Rs 1,000 installation charges (which I can use the gift coupons). Adding the remaining Rs 500 gift coupon, I get a Tata Sky hardware + 8 months of free subscription. All for using your Credit Card ! Wow! Man you got to love Credit Cards :-)

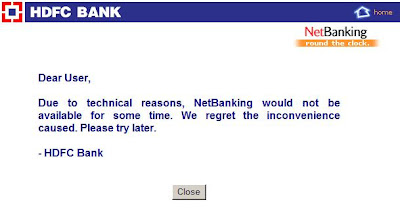

Round the clock?

Posted On Jul 2, 2007 at by Prakash G.R.I know internet banking provides round the clock services, but why should they have it on "this" particular page?

Related Links:

Special Message from HDFC

Bank anywhere

Posted On Jan 24, 2007 at by Prakash G.R.Few years back, I opened a PPF account with a SBI branch in Chennai. Today I approached a near by SBI branch in Bangalore to deposit some amount. They said that I can pay only in the branch where I opened. When I asked about "Anywhere Banking" ads, they said it applied only to Savings Account and not to PPF account. I enquired about changing the account to this branch. They said, it might take more than a month for that. Grrrrr.

Ok. Now what to do with the cash? I thought I'll deposit it back into my savings bank account which is with ICICI. I was surprised that they are not getting cash in the counter directly. Rather we need to put it inside a envelope; seal it and deposit it in the counter. They will later open it in a room with surveilance cameras; count the cash and deposit it in my account. Why such a stupid procedure? I asked what if the total amount I've mentioned in the envelope differs from the amount inside. They said they will ignore what I've mentioned in the envelope and update with the actual amount. If that is the case why should I count and update the denomination?

The worst thing, I have to deposit the amount in the same branch where I have the account. If not I've pay 0.5 % charge (with a minimum of Rs 150/-)

That is the truth of "Bank Anywhere". hmmm. Look into more details into "* conditions apply" in the ads.

HDFC Bank …

Posted On Jan 6, 2007 at by Prakash G.R.Banking and Finance sector customers are the risky ones for an IT Company and as I know they charge a huge amount for any project. Still there will be silly errors. Today when I logged into my HDFC Bank's Savings account, I had a message:

Since I've applied for an address change, I thought it might be something related to it. But when I clicked it, I got:

Hmmm. I didn't know that it was really a very special message !!!

ICICI bank is flooded !!!

Posted On Dec 22, 2006 at by Prakash G.R.Today morning I got a mail from ICICI Direct. The content is:

Dear Customer,

We regret to inform you that the documents and proofs of identity and address given by you at the time of account opening have been fully damaged by flooding in the storage areas caused by heavy rains. The natural disaster was most unfortunate.Time bound resubmission/re-execution of the documents is necessary for compliance to various regulatory and legal requirements and to keep the account operational.

In order to complete this formality, you need to submit an account opening form and other documents. The Bank branches listed below will remain open on 23rd and 24th December to help you complete the documentation in time.

While we regret this imposition on you, we urge you to complete the formalities as soon as possible.

We state that no charges would be collected from you for re-submission of the forms.

We earnestly seek your co-operation in helping us serve you better.

Sincerely,

Customer Service

ICICIdirect.com

I initially thought that it might be a phishing attack, but then it seemed to be genuine. I wonder how the nation's largest private sector bank is handling documents of high importance. They are not ready to come and collect but expect me go to their branch and submit the documents. Worst, they expect me to do it on a long weekend and send a mail on that friday. I'm not going to do it. Let me see how far it goes.

BTW, am I the only one whose documents were lost in the flood? Did anyone else get this mail?

[Update 26-Dec-06]

From what Jaganath said in the comment and many more people ending at this blog entry for search terms like "icici last documents flood", it looks like I'm not the only one whose document is lost. After the mail, I've another mail and few sms reminding me to visit the bank and submit the details. I replied the mail saying that its the bank's mistake that they didn't keep the documents safe and they should come back to me and collect the documents. No reply so far.

When we want to open an account these guys are behind us. They will send persons to your office or home or whereever you want to get all those documents. The treatment is royal. Once you are a customer then things are different. They charge you for everything (Citibank charged me Rs 50/- for withdrawing money from the bank counter when I lost my ATM card). I've decided not to visit the office and produce the documents rather ask them to come and collect it, since loosing the documents is their mistake. Let me see how far it goes.